The company was incorporated as a private limited company on March 28, 2001. was converted into a public unlisted company in 2007, while in 2014 Hascol was listed on the Pakistan Stock Exchange Limited The firm was granted an Oil Marketing License by the Government of Pakistan in 2005 for the purchase, storage and sale of petroleum products like high speed diesel, gasoline, fuel oil and FUCHS lubricants.

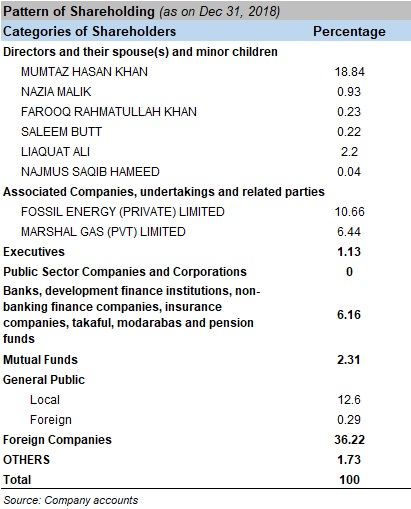

In November 2015, the global oil trader, Vitol acquired 15 percent of HASCOL and another 10 percent in 2016, which made Vitol Dubai Limited the largest shareholder in the company. The other prominent shareholders in the company include local firms like Fossil Energy (Pvt.) Limited and Marshal Gas (Pvt.) Limited; and Mumtaz Hasan Khan who is the Chairman and the Director of the company.

HASCOL has a strategic license agreement with FUCHS Middle East (FOMEL), an associate of FUCHS Petrolub based in Germany, to represent the brand in Pakistan. It also markets LPG through its retail network for the automotive sector, and currently there are 15 AutoMax LPG stations across Pakistan in various stages of approval with the Government of Pakistan. The company plans to market LPG for domestic consumers and to develop several auto gas LPG stations across the country in the coming years.

HASCOL and Vitol have also entered into a joint venture company for marketing of LNG in the country with 30/70 percent share, respectively. HASCOL has also signed a Technical Services Agreement with Vitol Aviation to enable the firm to start fuelling aircrafts at Karachi, Lahore and Islamabad airports in the country.

Past performance

Hascol Petroleum Limited has gained a lot of prominence in the downstream oil and gas sector in no time by capitalising on the growth in POL demand in recent years with a focus on retail side. The investment in the storage side came at the right time where the company in collaboration with its international sponsor Vitol has added 232,000 cubic metres of oil storage capacity at Port Qasim, taking it to 28 days from 16 days previously.

The OMC has witnessed aggressive expansion in the storage facilities and volumetric sales. It has overtaken its competitors to become the second largest OMC in Pakistan in terms of volumes with a CAGR of 54 percent over 2011-16. The company has opened 495 retail outlets in Pakistan till March 31, 2019, as per the information available on the website. The table shows the province-wise breakup where their concentration continues to be in Punjab and Sindh.

A look at the company's performance has been sanguine in the last couple of years where its volumes increased by almost 46 percent in FY16 with improved net margins during the year. Key highlights for 2016 included the commissioning of ZY terminal at Keamari, which has enabled the company to import larger volumes of motor gasoline; and the completion of a storage facility at Mehmood Kot, which will enable the firm to receive diesel directly via pipeline from Karachi. The company also set up Hascol Terminals Limited with Vitol for 200,000 metric tons of storage at Port Qasim.

Expansion of its supply chain network continued in 2017. Increased volumetric sales of retail fuels continued where the company's share in white oil reached 12 percent in 2017 versus 2 percent four years ago. During the year, HASCOL also started a chemical business for importing bulk chemicals and supplying to end users. Its volumes increased by 39 percent year-on-year in CY17, with revenues growing by75 percent, and gross profit growing by 44 percent, year-on-year. Earnings for the year increased by over 15 percent, year-on-year. The same year, HASCOL also announced right issue of 20 percent to fund upcoming projects like development of storage facilities, retail outlets and lube oil and grease blending plant.

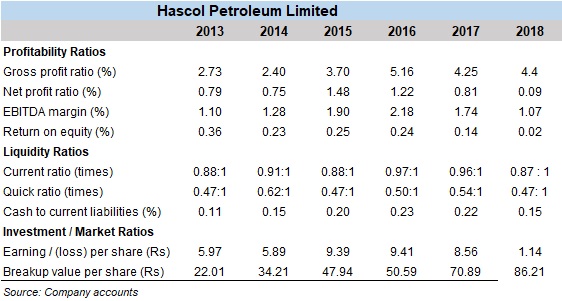

In 2018, HASCOL's performance was bitten by high exchange losses. This can also be seen from the stock's performance against the benchmark. The OMC's profits fell by 85 percent, year-on-year, and the one main factor behind the decline in earnings was exchange losses as a result of the currency depreciation. However, other factors too contributed to the dismal performance of the company.

Revenues increased by 35 percent; however, the increase came from higher prices of retail fuels and not growth in volumes. This decline in volumes for the company came as a general downtrend in the consumption patterns in the country as well as increasing competition. Higher margins earned on retail fuels resulted in growth in gross profit by 39 percent, year-on-year in 2018. However, the company's higher exchange losses along with finance cost due to increased borrowings for capex as well as working capital needs eroded the growth in earnings.

FY19 and beyond

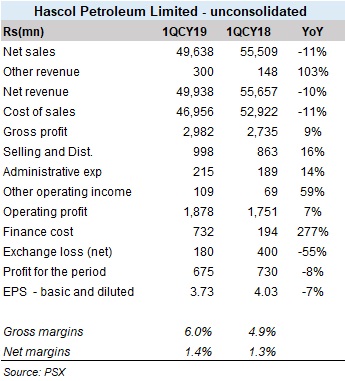

Things improved a bit for HASCOL in 1QCY19. Though an 8 percent year-on-year decline in earnings for 1QCY19 is nothing to boast about, the oil marketing company posted a comeback from its quarter-on-quarter declining performance. The 4QCY18 was bleeding for HASCOL as the company posted a loss of Rs1.3 billion, and compared to that, earnings of Rs675 million 1QCY19 was a recovery.

The OMC's revenues declined by 11 percent year-on-year, and volumetric growth too remained sluggish; key fuels like furnace oil, HSD and motor gasoline volumes slipped by 39 percent, 26 percent, and 10 percent, respectively. However, inventory gains during the quarter lifted gross margins and hence the net margins.

Also, the finance cost increased by over three times due long term financing obtained back in December 2018 along with higher interest rate environment. On the exchange loss side, the situation was better due to only 1 percent currency depreciation during 1QCY19.

While HASCOL ended up with a decline in its earnings growth in its profits for 1QCY19, maybe the company is out of the loss. The company is hopeful to commission its lube blending plant in June this year, which will give a boost to its lube sales. It is also aggressively developing its storage infrastructure and retail network.