Besides oil and gas, POL is also involved in the production of solvent oil, sulphur, and LPG. It markets LPG under its brand name POLGAS as well as its subsidiary, CAPGAS (Private) Limited. POL also has a pipeline network for the transport of crude oil to Attock Refinery Limited.

The associate group companies include Attock Refinery Limited, National Refinery Limited, Attock Petroleum Limited, Attock Cement Limited, Attock Gen. Limited, and Attock Information Technology Services.

More than half of the company's shareholding rests with the Attock Oil Company (AOC), which is the group. Another shareholder with more than 5 percent of the shareholding is the State Life Insurance Corporation of Pakistan. A category-wise breakup of the shareholding is shown in the illustration.

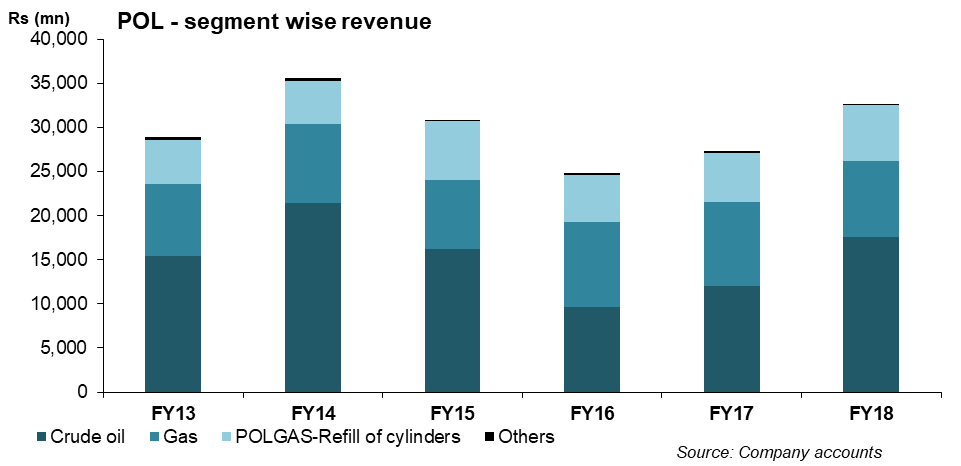

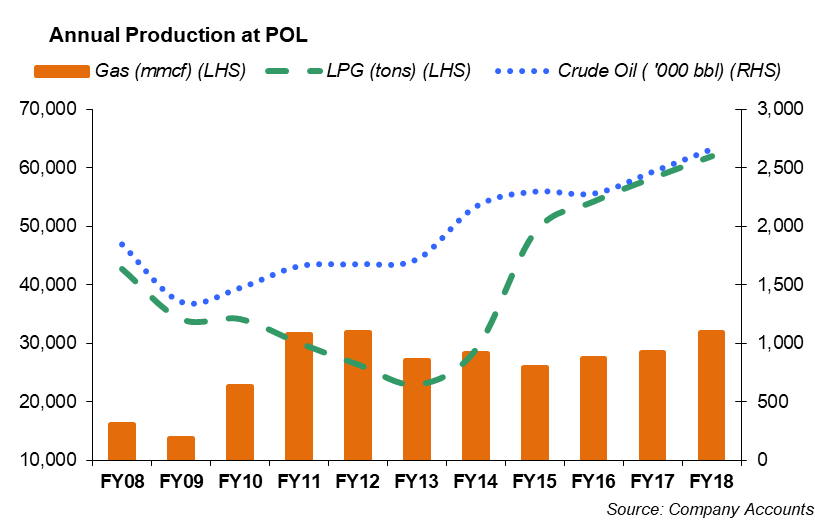

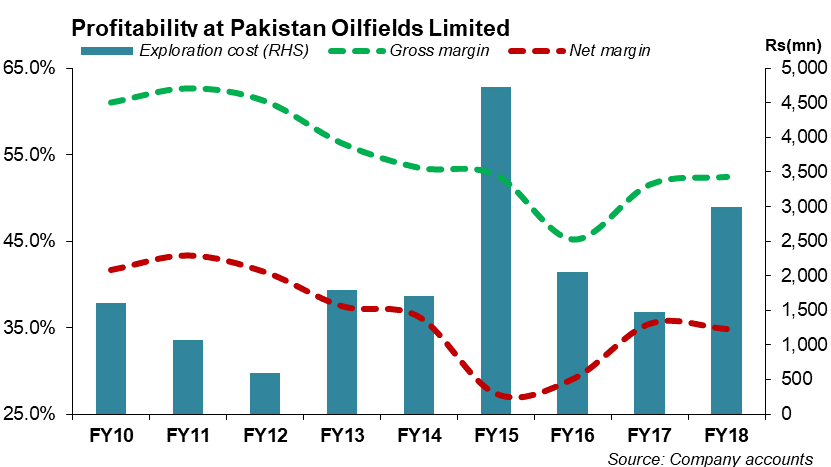

POL in the recent past Historically, POL has been an oil heavy company: Revenues from crude oil have accounted for 55-60 percent in the past, while natural gas has accounted for 20-25 percent of the total sales; POL's performance in FY15 was affected by the declining crude oil prices; and while sales were affected by lower prices, the excessively higher exploration and prospecting expenditure in year further cut the earnings for FY15. Growth on the volumetric front was positive, especially that of crude oil. Similarly, LPG production also increased. In FY15, earnings declined by around 34percent, year-on-year.

Restricted growth in the top-line and the bottom-line for POL continued in FY16 as low crude oil prices remained the highlight of the year. The E&P firm's revenues depicted not only a an predictable decline due to weaker international crude oil prices, but also due to 2-3 percent decline in POL's crude oil production from its key fields like Mamekhel and Manzalai fields. Some relief to the bottom-line came from lower exploration and prospecting expenditure versus the excessively high expense in FY15. In FY16, earnings decline by 14 percent, year-on-year.

FY17 was a better year for the E&P sector as the oil prices took a turn. POL's revenues were up by 10 percent year-on-year after continuously declining for the two years. Similarly, POL's bottom-line in FY17 was up by 34 percent, year-on-year, and that too after falling for the last two years. Exploration costs remained under control too. However, lower exploration cost does not necessarily reflect positively on a firm as it also points towards lower exploration and drilling activity. FY17, POL's activity included spudding only one exploration well. The company also witnessed a drop in production flows from its key field: Tal Block.

FY18 operational and financial performance In FY18, POL made four new exploratory successes, which included Jandial that has promising prospects. Three of its development wells were also successful in the fiscal year.

On the financial side, the company's revenues increased by 19.74 percent year-on-year, while the earnings saw a growth of 17.6 percent, year-on-year in FY18. Increase in revenues came from 7.83 percent higher crude oil production, which was the highest production in the last ten years, along with 27.7 percent increase in average crude oil price. Gas and LPG production too increased by 12.33 percent, and 6.36 percent, respectively during the year.

As per the annual accounts for FY18, increase in exploration costs for the year was mainly due to seismic acquisition of Balkassar Lease, DG Khan and Gurgalot block, and dry and abandoned wells and some irrecoverable costs. Increase in other operating income came from exchange gains due to depreciating currency.

2019 and beyond FY19 for POL began rather excitingly. The company's revenues were up by 46 percent, year-on-year and the earnings increased by over 50 percent, year-on-year in 1QFY19. Growth in earnings came primarily from the higher crude oil prices, which were up by 48 percent, year-on-year. However, volumes for crude oil remained flat in 1QFY19. The company's volumes for gas showed an increase of over 9 percent, year-on-year. Other factors that led to higher bottom-line were the increase in other income from the currency depreciation. Increase in earnings came despite higher operating costs, higher amortization of development and decommissioning costs, and significantly higher exploration expense

According to the company's annual report for FY18, wells will be spudded out of which two wells are exploratory, besides two wells that were being drilled at that time (one was exploratory).

=============================================================================

Pakistan Oilfields Limited

=============================================================================

Rs (mn) 1QFY19 1QFY18 YoY

=============================================================================

Net Sales 10,570 7,241 46%

Operating cost 2,779 1,973 41%

Excise duty and development surcharge 78 71 10%

Royalty 1,084 662 64%

Amortization of development and decommissioning costs 774 512 51%

Cross Profit 5856 4,022 46%

Exploration and prospecting expenditure 731 272 168%

Admin expense 57 38 53%

Finance cost 402 188 113%

Other charges 372 244 52%

Other income 841 249 238%

Profit before Tax 5,134 3,528 46%

Taxation 1,267 994 27%

Profit after Tax 3,867 2,534 53%

EPS (Rs/share) 13.62 8.93 53%

Cross margins 55.40% 55.55%

Net margins 36.58% 35.00%

=============================================================================

Source: PSX

=============================================================================

POL- Pattern of shareholding (As on June 30, 2018)

=============================================================================

Categories of Shareholders Percentage

=============================================================================

Banks & Financial Institutions 6.90%

Associated Companies 52.86%

Public Sector Companies 1.14%

Modaraba Companies 0.00%

Mutual Funds 9.16%

Investment Companies 2.15%

Insurance Companies 8.97%

Individuals 15.91%

Others

Employees Old Age Benefits Institution 1.23%

Deputy Administrator Abandoned Properties 0.00%

Employees Pension/Provident Fund 0.87%

Charitable Trusts & Foundation 0.79%

=============================================================================

Total 100.00%

=============================================================================

Shareholders holding 05% or more voting interest

The Attock Oil Company Limited (also shown under associated compani 52.75%

State Life Insurance Corp. of Pakistan (also shown under insurance 5.67%

=============================================================================

Source: Company accounts